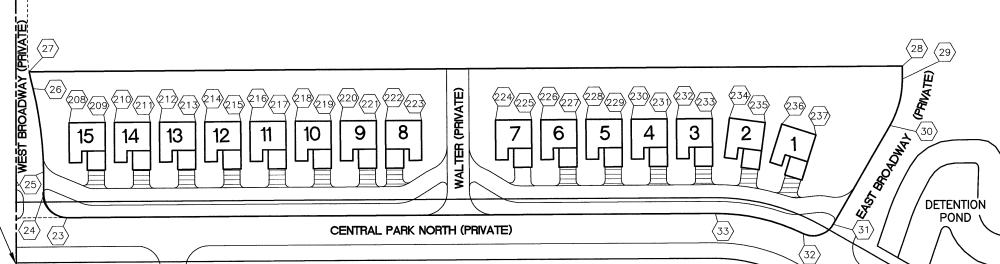

The "Carpenters Pension Trust Fund - Detroit & Vicinity"

(CPTF) acquired ownership of 63 incomplete

units at the Manors at Central Park Condominiums from "Sable

Realty Ventures - Shelby I Limited Partnership" in August of 2007. Sixteen of those

incomplete units were already under construction and the CPTF

hired Lombardo Homes to finish and sell them (those were in addition to the incomplete Units 1-14 along North Central Park that Lombardo Homes bought directly from Sable Realty Ventures in May of 2009 and upon which they subsequently built thirteen detached condos).

As of December 2011,

the CPTF stll owns 47 incomplete units and has no plans to begin

construction on any of them in the forseeable future. The CPTF also controls two of the three seats

on the Board of Directors of the Manors at Central Park

Condominium Association. Full control of the Board has not yet

transitioned to the co-owners and the third seat has been held by a duy-elected

co-owner of a completed unit since January 2008.

In accordance with Federal Law, the CPTF employs a Qualified Pension Assets Manager (QPAM) to manage their investments for them, including the

47 incomplete units at the Manors at Central Park Condominiums as

well as the operation of the Manors at Central Park Condominium

Association. Titanium Real Estate Advisors of

Chicago, IL has been the QPAM for the CPTF since August 2010 (prior to that Fifth Third Bank had been their QPAM).

Once full control of the Board is

transitioned to the co-owners (planned

to occur at the 2012 Annual Meeting on Jan. 18, 2012), Titanium will no longer be involved in the operation of the Manors at Central Park Condominium

Association. However, Titanium and the CPTF will still remain responsible for maintaining the appearance of their incomplete units and are also responsible for paying any Special Assessments levied against their units for the completion of unfinished site improvements such as the final layer of asphalt pavement on our streets.

At the beginning of its 2007 plan year, the CPTF was 67%

funded [see pg. 3 of this

document], meaning that the value of its assets ($1.08

billion) were worth about two-thirds the present value of all

accrued benefits being promised to the pension plan participants

and beneficiaries ($1.61 billion). During the 2008 plan year, its

funding fell below the Pension Protection Act's 65%

"critical" threshold, placing

it in the "red" zone and initiating the creation of a

rehabilitation plan to bring it up to the 80% funded level

("green" zone) by the 2019 plan year [see pp. 4-6 of this

document].

In a September 2009 report, Moody's Corporation

analyzed the funding levels of the 108 largest union pension

plans in the United States, which included the CPTF. A list of

those pension plans and their funding percentage is reproduced here.

Their report ranked the CPTF in 104th place, identifying it as

being only 41.4% funded at that time.

In 2010, the CPTF was again assessed as "critical" and placed in the "red" zone [see pg. 1 of this

document].

The CPTF is a multiemployer, defined benefit pension plan that

is safeguarded by the Pension

Benefit Guarantee Corporation (PBCG) under their Multiemployer

Insurance Program. The PBCG is a Government

Sponsored Enterprise, similar to Fannie Mae and Freddie Mac

in that it was created by the US Congress and it carries the

implicit financial backing of the US Government.

If the financial

status of the CPTF should deteriorate to the point of insolvency,

the PBGC will step in and mandate that they reduce their pension

benefit payments to a level that is supportable by the current

value of its assets. The PBGC also has the authority to provide

financial assistance to the insolvent pension plan and to also

exercise operating authority over the plan until all loans are

repaid.

In the event that the CPTF should become insolvent, more than likely the PBGC would then have the final say on all decisions regarding the CPTF's expenditures at the Manors at Central Park, including the payment of Special Assessments.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}